.svg)

.svg)

The global insurance industry is navigating not a single storm, but a convergence of forces creating a "perfect storm" of unprecedented complexity. Volatile macroeconomic pressures, including persistent inflation and uncertain investment returns, are squeezing margins and elevating operational expenses. Simultaneously, the risk landscape is being fundamentally reshaped by phenomena like climate change, which is creating new patterns of catastrophic loss, and the ever-present threat of sophisticated cyberattacks targeting the vast repositories of sensitive data that insurers hold. Compounding these external pressures are the radically evolving expectations of a new generation of customers, who demand seamless, personalized, and instantaneous digital experiences, a standard set by tech giants outside the industry. In this environment, incremental change is no longer a viable strategy for survival, let alone market leadership. The industry has arrived at a fundamental crossroads where its traditional foundations are being tested as never before.

This report will demonstrate that by 2030, the line separating market leaders from laggards will be drawn not by product or price alone, but by the underlying architecture of their business. The winners will be those who shed the immense liability of their legacy systems and embrace a new operating model: the connected, API-driven ecosystem. This is not merely a technological upgrade; it is a fundamental reinvention of how insurance value is created, distributed, and delivered. The future belongs to those who can build and participate in these interconnected networks, leveraging data and technology to achieve a level of agility, efficiency, and customer-centricity that is impossible within the confines of traditional, monolithic structures.

To substantiate this imperative, this analysis will first diagnose the core liability holding the industry back—its aging, inflexible, and costly technological infrastructure. It will then define the new competitive paradigm of the API-driven ecosystem, illustrating its transformative impact across every core insurance function, from underwriting and claims to distribution and customer service. Finally, it will present the strategic pathway for carriers to make this essential transition efficiently and effectively, highlighting the role of platform-based models in accelerating this journey. The choice facing industry leaders is stark: remain anchored to the past or build the architecture of the future.

For decades, the insurance industry's core systems were considered assets—robust, reliable engines that powered the business. Today, for a vast number of carriers, they have become the single greatest liability. These monolithic, inflexible systems are no longer fit for purpose in a dynamic, digital-first world. They are not just inefficient; they actively prevent carriers from responding to the market's existential threats and opportunities. This aging infrastructure is a profound drain on capital, a formidable barrier to innovation, and a growing risk to the business itself. Clinging to these systems is no longer a matter of prudence; it is a direct threat to future viability.

.png)

The most immediate and quantifiable damage inflicted by legacy systems is their immense financial weight. These systems consume a disproportionate share of capital that is desperately needed for innovation, growth, and competitive differentiation. A staggering 70% of a typical insurer's annual IT budget is spent not on creating new value, but simply on maintaining these outdated systems. This is not a static cost; research shows that maintenance expenses for outdated systems can increase by nearly 15% for each year they remain in use, creating a compounding financial burden.

This financial drain directly impacts profitability and competitiveness. Analysis reveals that IT costs per policy can be as much as 41% higher on legacy platforms compared to modern ones, a differential that puts direct pressure on an insurer's combined ratio. This internal cost pressure is dangerously amplified by external macroeconomic forces. High economic and social inflation are driving up the cost of claims for everything from auto parts to construction materials and legal defense, while rising reinsurance costs are further squeezing margins. In this environment, many insurers are already operating on a knife's edge, with the industry in the first half of 2023 spending 104.3 cents in claims and expenses for every 100 cents of premium collected.

This situation creates a destructive feedback loop. As legacy systems age, they demand more resources for maintenance, leaving even less capital available for modernization projects. This lack of investment in new technology causes the insurer to fall further behind more agile, digitally native competitors, leading to a loss of market share and profitability. This, in turn, further constrains the budget available for transformation. It is a self-reinforcing cycle of technological and competitive decline, where the cost of maintaining the past actively prohibits investment in the future.

Beyond the direct financial costs, legacy systems impose a crippling operational tax on the entire organization. They are characterized by manual, often paper-based processes and siloed data architectures that result in slow, error-prone workflows. Even a task as simple as a customer address change can become a complex, multi-step process involving phone calls and manual forms, a stark contrast to the one-click updates customers expect elsewhere.

This inherent rigidity makes it nearly impossible for insurers to operate with the agility the modern market demands. The process of launching a new insurance product on a legacy platform can take months, if not more than a year, and cost millions of dollars. In a market where new risks emerge rapidly and customer preferences shift constantly, this glacial time-to-market is a fatal competitive disadvantage, putting insurers at risk of falling behind competitors who can deploy updates and new products in a fraction of the time.

Furthermore, these systems were designed in an era before the strategic value of data was fully understood. As a result, critical data often resides in disparate, incompatible legacy systems, making it nearly impossible to gain a holistic, 360-degree view of customers or broader market trends. This creation of "data silos" is not a minor inconvenience; it directly hinders the most critical functions of the business. It prevents accurate, data-driven risk assessment, makes personalized pricing difficult, and severely limits the ability to implement effective, enterprise-wide fraud detection strategies.

The financial and operational deficiencies of legacy technology translate directly into severe strategic consequences that impact every facet of the business, from customer relationships to cybersecurity.

First, these systems are a primary driver of poor customer experience. Today's consumers, accustomed to the seamless, personalized, and instant service from companies like Amazon, expect the same from their insurers. Legacy systems, with their clunky interfaces, limited self-service options, and slow response times, deliver the exact opposite. This friction-filled experience leads directly to customer frustration and, ultimately, churn, as policyholders seek out more modern and responsive providers. This technical failure becomes a business failure, eroding the very trust the industry is built on. Public opinion of the insurance sector is already at an all-time low, fueled by perceptions of delayed claims processing, high premiums, and a lack of transparency. Legacy systems are a root cause of these issues: their slow, manual processes create the delays, their high operating costs contribute to the premiums, and their siloed data prevents the transparency customers demand.

Second, legacy systems represent a significant and growing security and compliance risk. Older platforms often lack the robust, modern security features required to defend against sophisticated cyber threats, leaving valuable customer data and core business operations vulnerable to breaches. Their rigid architecture also makes it incredibly difficult and expensive to adapt to new and evolving regulatory requirements, such as stricter data privacy laws or more detailed financial reporting standards.

Finally, reliance on archaic technology creates a critical talent drain. The pool of IT professionals with the specialized skills needed to maintain these systems—written in aging languages like COBOL or even 370 Assembler—is rapidly shrinking and becoming more expensive. Simultaneously, these outdated platforms make it nearly impossible to attract and retain the next generation of highly skilled tech talent. The best and brightest engineers, data scientists, and developers want to work with cutting-edge technologies like AI and cloud platforms, not support "how we've always done it" processes on decades-old infrastructure. This creates a talent gap that further widens the chasm between legacy-bound insurers and their digitally native competitors.

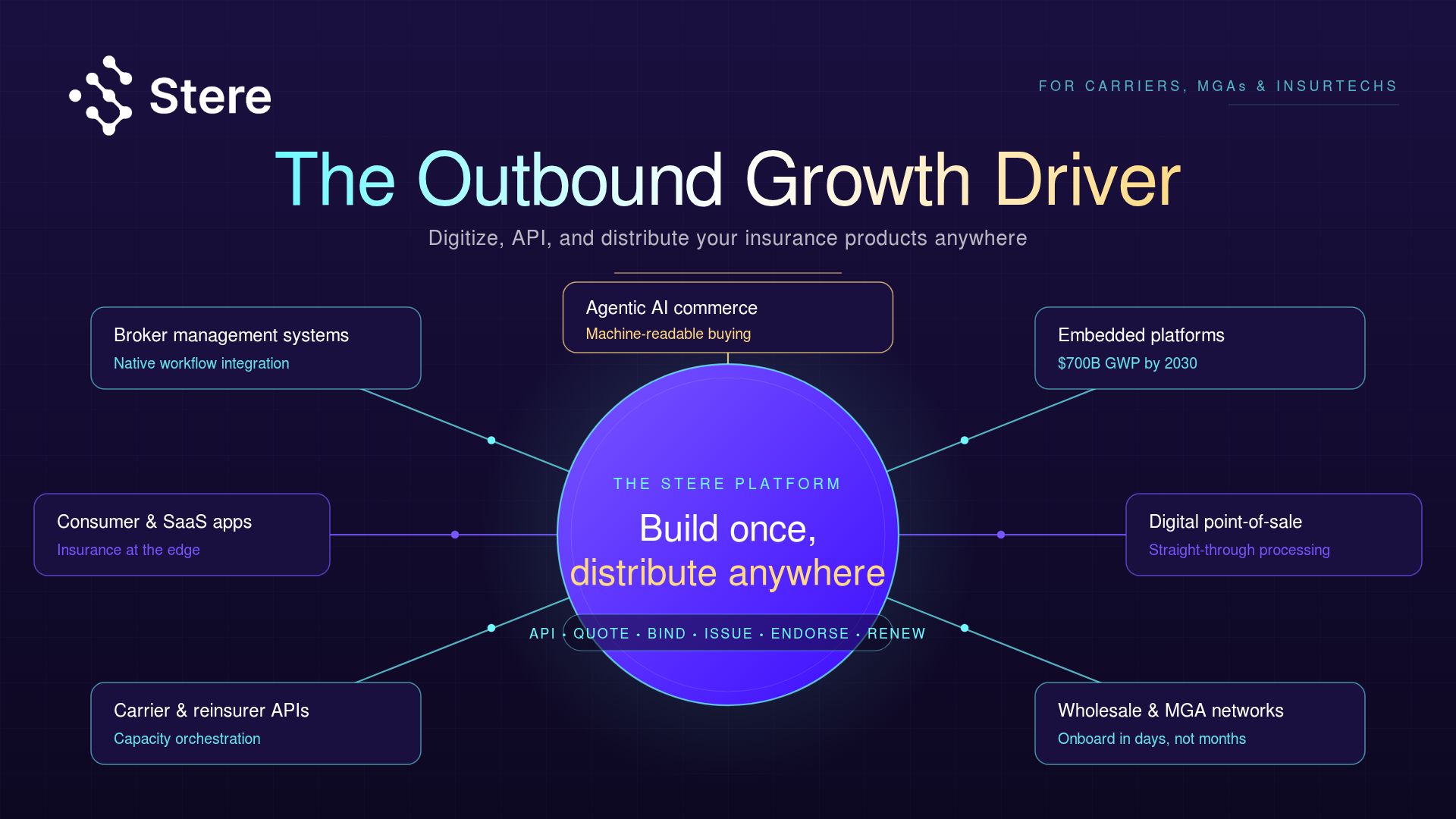

The antidote to the closed, brittle, and siloed nature of legacy systems is the open, flexible, and interconnected model of the digital ecosystem. This new competitive paradigm is not about replacing one monolithic system with another; it is about creating a dynamic network of interconnected capabilities, partners, and data sources. The fundamental technology that unlocks this model and serves as its connective tissue is the Application Programming Interface (API). Embracing an API-driven architecture (internal and externally) allows insurers and MGAs to transcend the limitations of their internal systems and participate in a much broader value-creation network.

A digital insurance ecosystem is an integrated framework of technologies, services, and partnerships that enables seamless, real-time collaboration between an insurer and a diverse range of stakeholders. This network can include traditional partners like agents, brokers, Managing General Agents (MGAs), and reinsurers, as well as new players such as insurtech startups, third-party data providers, and even non-insurance service providers from adjacent industries.

This model represents a profound strategic shift. It moves the insurer or MGA away from being a monolithic, vertically integrated provider of a limited set of products and toward becoming an orchestrator or a key participant in a broader network designed to serve the holistic needs of the customer. Instead of only thinking about selling a car insurance policy, for example, an ecosystem-minded insurer thinks about participating in the entire "mobility" ecosystem, offering coverage seamlessly at the point of a car purchase, through a ride-sharing app, or as part of a vehicle subscription service. This approach allows insurers to meet customers where they are, embedding protection directly into their life and business activities.

APIs are the technical enablers of this ecosystem vision. An API is a set of defined rules and protocols that allows different software applications to communicate with each other, sharing data and functionality in a secure and standardized way. They act as the "digital bridges" or the "digital nervous system" that connects an insurer's core systems—whether modern or legacy—to the outside world and to each other.

The power of APIs lies in their ability to abstract complexity. Instead of undertaking massive, complex, and bespoke integration projects to connect two systems (= creating custom integrations), APIs provide a clean, well-documented, and reusable method for interaction. This allows MGAs and insurers to "plug in" best-in-class services from third-party specialists rather than attempting to build every capability from scratch. For instance, an MGA can use an API to connect its products to various distribution channels to provide quote, bind, issue capabilities at the point of sale, another to bill the clients instantly without any human intervention, and a third to access real-time property data for underwriting. This API-led connectivity turns what were once repetitive and complex processes into highly reusable digital assets, dramatically increasing organizational productivity, speed, and agility.

This shift in technical architecture fundamentally changes the "build vs. buy" calculation that has long dominated IT strategy. Historically, if an insurer needed a new capability, the choice was binary: build it internally, which was slow and expensive, or buy a large, monolithic software package, which often created an integration nightmare with existing legacy systems. APIs introduce a third, far superior option: "connect." An insurer no longer needs to be an expert in every domain. It can focus its resources on its core competencies—such as underwriting complex risks or managing sophisticated claims—and use APIs to seamlessly integrate best-of-breed solutions for non-core functions. This transforms the business model from one of costly vertical integration to one of capital-efficient, networked specialization. The strategic focus shifts from "owning all the pieces" to "mastering the best connections," a far more scalable and resilient approach to growth in a rapidly changing market.

The philosophy underpinning this API-first world is a framework that leverages modern microservices, quick to deploy features and APIs to facilitate the accessing insurance products from MGAs and insurers. For brokers and customers this is empowering. It grants them greater ownership and efficiency, enabling them to more easily find the best fitted products, compare them, and have an instant experience.

Adopting an API-first strategy is more than just a technology decision; it becomes a powerful catalyst for profound cultural transformation. To expose data and services via APIs effectively, an organization is forced to break down the internal silos that have long plagued the industry, as data must be standardized and shared across departments before it can be made available to partners. This necessity fosters a culture of cross-functional collaboration. Furthermore, building and managing a network of API-based partnerships requires a new level of external collaboration, shifting the corporate mindset from insular to outward-looking. Most importantly, because APIs are designed to deliver a specific, valuable outcome to an end-user—whether that user is a customer, an agent, or a partner application—their development instills a deeply customer-centric mindset throughout the IT and business teams. In this way, an API strategy acts as a "Trojan Horse," driving the agile, collaborative, and customer-focused culture from the bottom up that industry leaders have been striving to instill from the top down for years.

The strategic shift to an API-driven ecosystem is not a theoretical exercise; it delivers tangible, quantifiable improvements across every core function of the insurance business. By breaking down data silos and enabling seamless connectivity, this new model transforms slow, manual, and inefficient processes into automated, data-driven, and highly responsive operations. This section provides a granular, evidence-based examination of this transformation across the insurance value chain.

.png)

The traditional underwriting process is notoriously manual, slow, and reliant on static, historical data points. Underwriters often spend as much as 30 to 40 percent of their time on low-value administrative tasks like rekeying data from different systems, rather than on high-value risk analysis. This legacy approach is not only inefficient but also increasingly inadequate for pricing the complex and dynamic risks of the modern world.

The ecosystem approach completely revolutionizes this function. It creates an automated, dynamic, and predictive underwriting engine. Through APIs, underwriters can connect to and ingest the insurance application and in parallel a vast array of real-time data sources that were previously inaccessible (i.e. data from IoT sensors on industrial equipment, telematics devices in vehicles, public and private property records, satellite imagery, and real-time weather feeds); apply underwriting and rating rules before even he/she sees the application. Advanced AI and machine learning models can then analyze risk with far greater precision, generating highly accurate, personalized quotes in seconds or minutes, not days or weeks.

The impact is profound. For most standard personal and small commercial lines, the manual underwriting process will effectively cease to exist by 2030, replaced by semi- automated, straight-through processing. This automation drives significant gains in both accuracy and efficiency. Studies have shown that insurers using modern Risk Assessment APIs have seen a 20% increase in underwriting accuracy, leading to better risk selection and improved profitability. AI implementation has already helped a third of underwriters gain better access to real-time data, fundamentally changing their workflow. This frees human underwriters from mundane data entry and allows them to evolve into more strategic roles, focusing on managing complex risks, refining the algorithms, and overseeing the performance of the overall underwriting portfolio.

Legacy policy administration is characterized by paper-heavy, high-friction processes and a limited number of distribution channels, which are neither profitable nor popular, creating a poor customer experience.

An API-driven ecosystem transforms both the product and its distribution. Modern Policy Management systems and their comprehensive APIs enable dynamic, digital-first policy lifecycle management. They allow for the instant creation of policies, automate the renewal process with timely notifications, and facilitate real-time modifications requested by the customer or agent. This digital backbone has enabled insurers using these APIs to achieve a 30% reduction in policy administration costs.

Even more transformative is the impact on distribution. APIs are the key enabler of efficient broker distribution, embedded/affinity distribution, as well as new distribution channels like AI platforms and through agentic flows. This strategy exponentially expands an MGA or insurer's reach. The market is shifting rapidly in this direction, with forecasts predicting that by 2028, more than 30% of all insurance transactions will run through these embedded channels. This new distribution reality, combined with the ability of Quote Generation APIs to deliver instant, accurate pricing, has been shown to drive a 25% increase in quote-to-sale conversion rates. Now we can implement Quote-Bind-Issue-Payment APIs to supercharge the potential of this approach.

For many customers, the claims experience is the ultimate moment of truth, and the traditional process is often slow, opaque, and adversarial, leading to frustration and eroding trust. It relies heavily on manual data collection, phone calls, and physical assessments, creating significant operational costs and delays.

The ecosystem model turns this experience on its head, creating a process that is fast, transparent, and increasingly proactive. APIs enable automated First Notice of Loss (FNOL) directly from connected devices; for example, a car's telematics system can automatically report an accident, or a smart water sensor in a home can report a leak. Customers can use their client portals/apps (or ask their AI agent) to initiate a claim instantly, submitting photos and videos of the damage directly from their phones. APIs then orchestrate the entire workflow, connecting to fraud detection systems that use AI to analyze the claim data, and linking to payment gateways to issue instant payouts for approved claims.

This technological shift has a dramatic impact on efficiency and customer satisfaction. Insurers leveraging Claims Processing APIs have documented a 40% reduction in claims processing time. The use of Data Analytics APIs to spot irregularities has led to a 35% reduction in fraudulent claims, generating substantial cost savings. Ultimately, this allows the industry to shift its focus from simply compensating for losses to actively preventing them, using real-time data to alert customers to risks before they result in a claim.

The traditional insurer-customer relationship is transactional, infrequent, and siloed. Interactions typically occur only at the point of sale, renewal, or claim, and the experience is often inconsistent across different channels (e.g., agent, call center, website).

An API-driven ecosystem enables a fundamental shift to a relationship that is continuous, relational, and truly omnichannel. APIs are the key to breaking down data silos and creating a single, unified view of the customer. This ensures a consistent and personalized experience, regardless of how the customer chooses to interact—whether on a mobile app, a website, through a chatbot, or speaking with a human agent. This seamless connectivity allows insurers to move beyond one-size-fits-all service to deliver true personalization, anticipating needs and offering relevant advice and products at key life moments.

The results are improved satisfaction and greater efficiency. The integration of intelligent chatbots and self-service portals via Customer Service APIs can reduce customer support costs by as much as 25% while maintaining high satisfaction ratings. More importantly, this model allows insurers to change the nature of their relationship with customers. Instead of only interacting when something goes wrong, they can provide continuous value through ancillary services, such as wellness programs that reward healthy habits or risk-alert systems that help prevent losses, thereby fostering deeper loyalty and rebuilding trust.

Recognizing the monumental challenge of dismantling decades-old legacy systems and building a new digital ecosystem from the ground up, a new and powerful model has emerged to accelerate this transformation: Insurance-as-a-Service (IaaS). This model provides carriers, MGAs, and even non-insurance brands with a ready-made, API-first platform, effectively allowing them to leapfrog the most painful and expensive stages of modernization. By leveraging an IaaS platform, companies can immediately begin to operate and compete in the digital-first world, bypassing the risks and delays of a traditional "rip and replace" project.

In the context of the insurance industry, Insurance-as-a-Service is a business and technology model where a provider offers a full-stack, cloud-based insurance platform that includes all the necessary components to run an insurance program—such as policy administration, claims management, billing, and underwriting tools—all accessible via a robust set of APIs. It is crucial to distinguish this from the more generic term "Infrastructure-as-a-Service" (IaaS) in cloud computing, which typically refers only to the provision of virtualized computing infrastructure like servers and storage. Insurance-as-a-Service is far more comprehensive; it is an end-to-end business platform, a complete "insurance company in a box" or “MGA in a box”

This model enables any company, whether it's an incumbent carrier looking to launch a new digital brand, an MGA wanting to scale, or a non-insurance company aiming to embed protection into its products, to launch a fully digital insurance offering quickly and cost-effectively. The IaaS provider handles the underlying technology, compliance, and sometimes operational complexities, allowing the client to focus on product design, marketing, and customer relationships.

The strategic advantages of adopting an IaaS platform are compelling and directly address the primary pain points of legacy-bound insurers.

The strategic logic of the IaaS model is being overwhelmingly validated by the market. The global Insurance-as-a-Service market, valued at US30.4billion in 2024,is projected to experience explosive growth, reaching an estimated US624.9 billion by 2034. This represents a compound annual growth rate (CAGR) of a staggering 35.3%. This rapid adoption is driven by the clear and compelling benefits the model offers, including reduced operational costs, scalable services, and the ability to deliver the enhanced customer engagement that modern consumers demand. The leading companies in this space are those that provide comprehensive, end-to-end solutions that integrate all core insurance functions into a single, seamless digital platform.

The emergence of IaaS platforms fundamentally democratizes innovation within the insurance market. Historically, the high barriers to entry—the immense capital required for technology, regulatory licensing, and building carrier relationships—meant that launching a new insurance venture was the exclusive domain of large, established incumbents. IaaS platforms shatter these barriers. A small, innovative team at an MGA or even a startup can now partner with an IaaS provider to gain immediate access to enterprise-grade technology and, in some cases, "rent" underwriting capacity from carriers already on the platform. This levels the playing field, allowing smaller, more agile players to bring new ideas and products to market faster and compete effectively with the giants. This surge in competition will ultimately benefit the entire market, especially consumers, with more choice, better service, and more innovative products.

For large, incumbent carriers, the IaaS model offers a pragmatic solution to the perilous "rip and replace" problem. Instead of attempting a single, high-risk "big bang" migration off their legacy mainframes, they can use an IaaS platform as a strategic "legacy abstraction layer." This allows for a phased and much safer transformation journey. An insurer can start by using the platform to quickly launch new, digital-only products or enter new markets, generating fresh revenue streams and allowing their teams to learn how to operate in a modern, agile environment. Concurrently, they can use the platform's robust APIs to gradually "wrap" their existing legacy systems, creating a modern interface that hides the underlying complexity from customers and partners. Over time, core functions like policy administration or claims can be migrated from the legacy system to the new platform piece by piece, without disrupting the entire business. The IaaS platform thus acts as a vital bridge, allowing an insurer to gracefully transition from the past to the future without undertaking a catastrophic, all-or-nothing project.

The insurance industry has arrived at a definitive inflection point. The converging pressures of economic volatility, a rapidly evolving risk landscape, and unrelenting customer demands have created an environment where the status quo is no longer sustainable. The path forward, however, is becoming increasingly clear. The fundamental choice facing every insurance leader today is between being anchored to the past by the immense weight and cost of legacy technology, or embracing the speed, agility, and customer-centricity of a connected, API-driven future.

Clinging to outdated, monolithic systems is no longer a viable long-term strategy; it is a path of managed decline. These systems drain capital, stifle innovation, frustrate customers, and expose the organization to unacceptable risks. The single most critical strategic decision for insurance executives over the next five years will be the commitment to a new operating model—one built on a foundation of modern, flexible, and interconnected technology.

The winning formula for 2030 and beyond is unambiguous. The future belongs to those organizations that leverage platform-based, API-first technology to become truly digital and data-driven. This transformation is the key to unlocking profound operational efficiencies, enabling the rapid innovation of personalized products, and delivering the seamless, omnichannel experiences that customers now expect as standard. By shedding the liability of their legacy past and embracing the ecosystem of the future, insurers can not only weather the immediate storms but also position themselves to capture the enormous opportunities of a changing world, achieving scalable, profitable growth for the next decade and beyond.

.svg)

Copyright © 2024. All Rights Reserved